Can Disruptive Innovation Be Predicted?

Disruption Strategy

Figure 1: The course of disruptive innovation

(Source: Wikipedia)

Recently, Jill Lepore wrote a lengthy piece in the New Yorker magazine called, “The Disruption Machine: What the gospel of innovation gets wrong“. She spends most of the article taking Clayton Christensen’s theory, and his scholarship, to task. [Dr. Christensen responded in an interview with Drake Bennett of BloombergBusinessWeek.] She concludes that:

“Disruptive innovation is a theory about why businesses fail. It’s not more than that. It doesn’t explain change. It’s not a law of nature. It’s an artifact of history, an idea, forged in time; it’s the manufacture of a moment of upsetting and edgy uncertainty. Transfixed by change, it’s blind to continuity. It makes a very poor prophet.”

I disagree.

I will agree that the phrase “disruptive innovation” is overused and underdefined. (Christensen does give a detailed definition in his work, but people tend to overlook that and use the term somewhat indiscriminately.)

Over the last few years my research assistants Ashank Gupta, Naman Garg, and I have tried to develop a taxonomy of innovation that tried to strictly define “disruptive”. It is like trying to nail Jell-O to the wall. So for the purposes of this essay, we will take the dictionary definition of the word “disrupt”:

disrupt (dɪsˈrʌpt) — vb 1. ( tr ) to throw into turmoil or disorder (Source: World English Dictionary via dictionary.com)

With this definition in hand, I will argue that we CAN explain disruption as a solid theory of industry dynamics and, if not prophetic, at least a powerful predictive tool. We will draw on Christensen’s work in “The Innovator’s Dilemma” and “The Innovator’s Solution“, as well as Michael Porter’s Five Forces, Everett Rogers’ Theory of Diffusion, and some principles from W. Chan Kim and Renee Mauborgne’s “Blue Ocean Strategy“.

Figure 2: Overserved Customers Are Ripe for Disruptive Innovation

Christensen states, “[a low end] innovation that is disruptive allows a whole new population of consumers at the bottom of a market access to a product or service that was historically only accessible to consumers with a lot of money or a lot of skill”. (See more at his website.) I believe that a more general description would be that an “innovation is disruptive when an overserved set of customers is given reasonable access to an alternative or substitute offering that provides the necessary utility at an acceptable price.”

That said, as shown in Figure 1, the principle that buyers will typically adopt a new, potentially disruptive offering by trying it out on low importance “jobs to be done” before committing higher importance “jobs” rings true. (Think of cloud computing.)

The principle of the “overserved customer” is important. A key tenet of the theory is that the pace at which technology improves (via “sustaining” or incremental improvements) outpaces the growth in the capacity of the customer to absorb or use these improvements. More features get added to a product in order to justify a new model or higher price, but the customer isn’t deriving any additional benefit from these features. Understandably, at some point a sense of frustration builds, and the “overserved customer” begins looking for alternatives. In Christensen’s model, that alternative is the “low end disruption”.

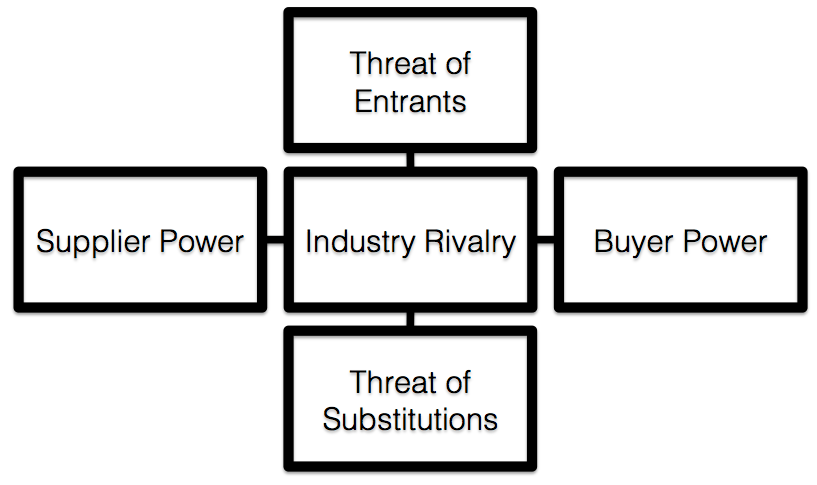

Figure 3: Porter’s Five Forces

Michael Porter, in his 1985 book “Competitive Advantage“, argued that there are five forces that collectively determine the profitability of an industry (See Figure 3.). In his models, the fundamental unit of study is the industry; recently, this has come under scrutiny by a school that argues that the customer and their needs are the fundamental unit, and that the firms that compete to serve this need define the industry. The distinction seems minor, but is important.

Existing, stable industries do face these (and other) forces that restrict the ability of a given firm to make money. Obviously, a high degree of rivalry — many firms with highly competitive or similar offers — will drive prices down and impede the ability to make a high profit. Likewise with high buyer or supplier power, where those parties dictate the terms on which they will do (substantial) business, or take their business elsewhere.

It is the threat of new entrants and the threat of substitute products with which we are concerned when it comes to disruptive innovation. Christensen defines “low end disruptions” (discussed earlier) which are essentially substitutes for doing a job that is already getting done. He also defines “new market innovations”, in which a new offering does a job that isn’t being done; essentially, a new entrant to an industry. (Think smartphones and tablets to the computer industry. Also, smartphones to the digital camera industry.)

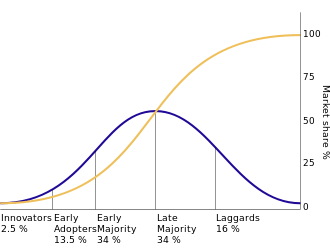

Figure 4: Diffusion of Innovation

(Source: Wikipedia)

In 1962, Everett Rogers introduced the concept of the “Diffusion of Innovation” (see Figure 4), the fundamental model behind technology adoption. He divided the world up into five populations, characterized by their willingness to adopt new things (or not). The labels are familiar: innovators, early adopters, early majority, late majority, and laggards (ouch!). [Geoffrey Moore famously inserted the “chasm” in between the early adopters and early majority, but that isn’t important here.]

When customers are exposed to new technology, this diffusion theory posits that some experimentally minded customers will avail themselves of the new offering just to see what it can do. If enough of them are successful, a slightly less adventurous crowd, seeking some early competitive advantage, will start to adopt. When the “early majority” start to adopt, a sea change is underway, and adoption becomes more like a stampede. This process is described well in Moore’s second book, “Inside the Tornado“, and the phenomenon more generally described in Malcolm Gladwell’s “The Tipping Point.”

The incumbent companies in the industry defined by Porter’s model are unable to react to this new offering, be it substitute or new entrant. Chan and Mauborgne describe that industry as a “red ocean”, where “industry boundaries are defined and accepted, and the competitive rules of the game are known.” (“Blue Ocean Strategy”, page 4) In red oceans, the nature of competition converges, and all players compete on the same factors for the same customers. The industries structural boundaries are fixed, and firms must compete within those boundaries. Investors value firms in the same industry based on the same factors for all companies. These factors severely limit the ability of incumbents to react.

This process has happened many times, on several scales. Chemical-based photography, with poster child Kodak, is a classic example. Craigslist disrupted the classified ads business and hence the newspaper industry. On a grander scale, the transistor and integrated circuit destroyed the vacuum tube-based electronics industry virtually overnight, as did the liquid crystal display to the cathode ray tube market. Solid state drives are displacing hard drives. I predict that electric motors, powered by batteries or fuel cells, will displace internal combustion engines according to the same principles.

When, exactly, the adoption of a new offering by customers of the incumbent companies becomes a stampede (or reaches critical mass, or hits the tipping point – choose your metaphor), is going to vary by type, scale, and characteristic of each unique industry.

But when (not if) it happens, the industry is thrown into turmoil or disorder.

It is disrupted.

No comments yet.